Most organizations pick a lending platform the wrong way. They go with the cheapest option, trust a flashy demo, or buy what a competitor is using. None of that is a strategy. And in microfinance, a bad software decision doesn't just waste money, it slows down your entire operation for months.

At ScriptLab, we've worked with enough MFIs, NBFCs, and fintech startups to know what separates software that actually helps from software that creates more problems than it solves. Here's what to check before signing anything.

What's Actually at Stake

Microfinance isn't a simple business. You're managing thousands of borrowers, field agents, repayment cycles, and compliance requirements all at once. A solid loan management system in India gives your team clarity and catches problems early. The wrong one creates dependency on workarounds and makes audits a nightmare. This isn't just a tech decision. It's an operations decision.

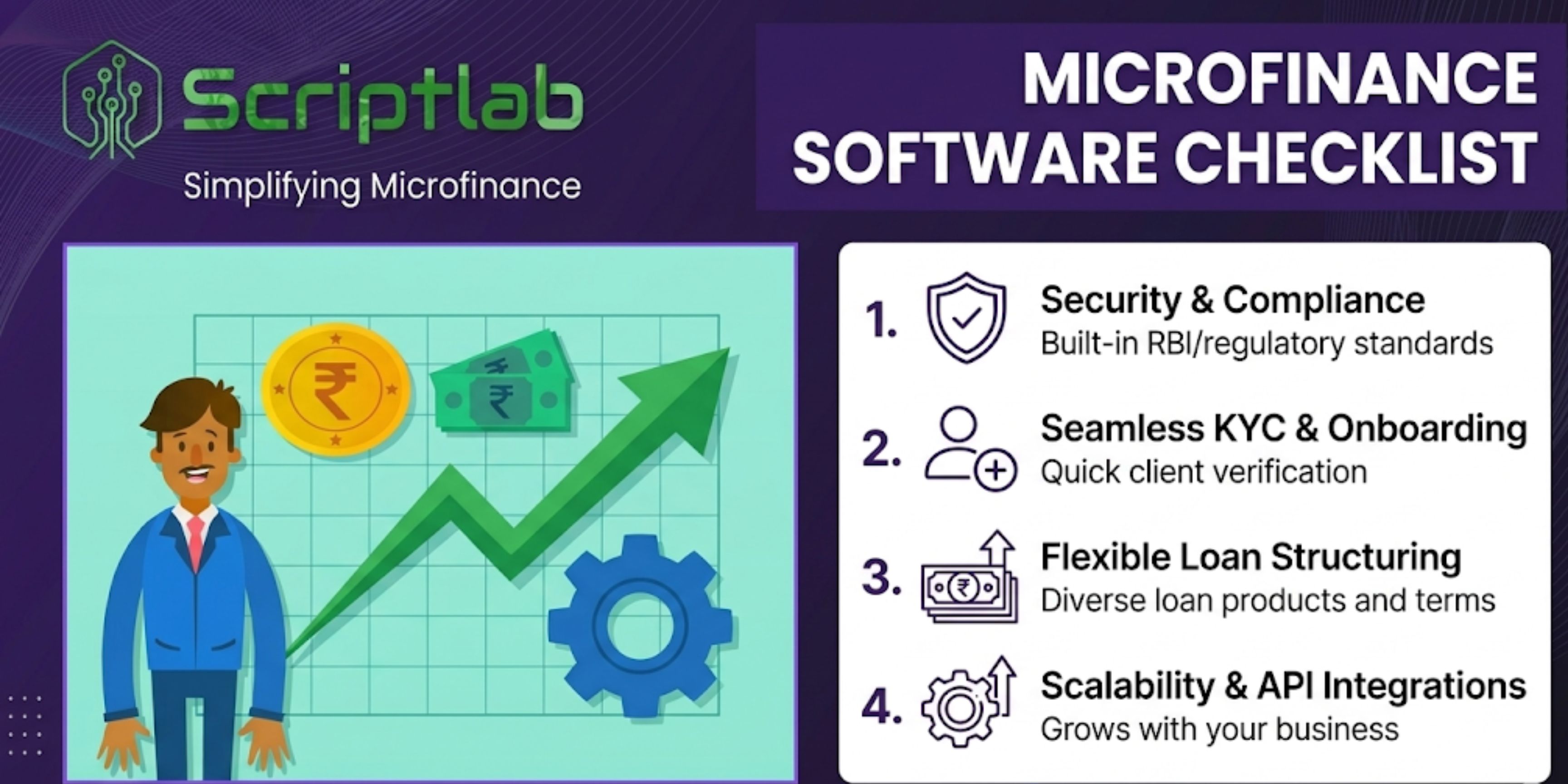

Eight Things Worth Checking

Start with the basics and make sure they actually work. The software must handle loan application workflows, EMI schedule generation, field and digital collection management, and KYC records without feeling clunky. If the demo feels awkward, daily operations will feel worse.

Compliance is non-negotiable. Aadhaar and PAN-based KYC, RBI reporting formats, audit trails, and proper data encryption. Don't just hear about these features during the sales call. Ask to see them working.

Look at how the interface feels for your actual team. Field officers need mobile accessibility. Managers need a clean dashboard. If the system requires weeks of training before someone can log a basic collection, that's a problem you'll live with every single day.

Collections are where microfinance lives or dies, so the EMI collection software needs to be genuinely strong. Offline and online modes, automated reminders, real-time repayment visibility. Anything weaker than that will quietly cost you recovery every month.

Check what the reporting looks like. Built-in reports on loan performance, collection efficiency, and financial summaries should be standard. If you're exporting everything to Excel just to understand your own portfolio, the software isn't doing its job.

Finally, think beyond today. Will the platform handle twice your current volume in two years? Does it integrate with payment gateways, WhatsApp tools, accounting software, and credit bureaus without manual workarounds? And who answers the phone when something breaks on a Monday morning? Post-sale support is part of what you're buying, not a bonus.

The Mistakes That Hurt the Most

Choosing based on price alone. Skipping the trial. Treating compliance as something to sort out after go-live. These three mistakes show up more than anything else, and they're all avoidable. Run the platform through your real workflows before committing. Ask hard questions. Demand proof, not promises.

Recent Post